Earned Value Management Gold Card

Download a printable version of this page.

The U.S. National Science Foundation Earned Value Management (EVM) Gold Card is a guideline document that outlines key earned-value concepts for managing NSF-funded projects that require earned value management.

It helps measure project performance in terms of cost, schedule and scope, allowing stakeholders and NSF to effectively monitor and control projects, ensuring adherence to established project goals.

On this page

On this page

Credit: U.S. National Science Foundation

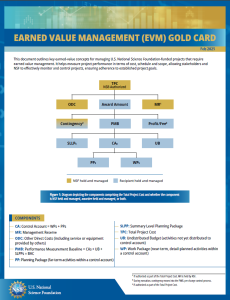

1 If authorized as part of the Total Project Cost. MR is held by NSF.

2 During execution, contingency moves into the PMB, per change control process.

3 If authorized as part of the Total Project Cost.

- Total Project Cost (TPC)*

- Other Direct Costs (ODC)*

- Management Reserve1*

- Award Amount§

- Contingency2*§

- Profit/fee1§

- Performance Measurement Baseline (PMB)3§

- Summary Level Planning Package (SLLPs)§

- Undistributed Budget (UB; activities not yet distributed to the control account)§

- Control Accounts (CA)4§

Planning Packages (PP; far-term activities within a control account)§

Work Packages (WP; near-term, detail-planned activities within a control account)§

* NSF held and managed.

§ Recipient held and managed.

1. If authorized as part of the total project cost.

2. During execution, contingency moves into the performance measurement baseline, per change control process.

3. Performance measurement baseline = CAs + UB + SLPPs = Budget at completion (BAC).

4. Control account = WP + PPs.

Components

- CA: Control Account = WPs +PPs

- MR: Management Reserve (held by NSF)

- ODC: Other Direct Costs (including service or equipment provided by others)

- PMB: Performance Measurement Baseline = CAs + UB + SLPPs = BAC

- PP: Planning Package (far-term activities within a control account)

- SLPP: Summary Level Planning Package

- TPC: Total Project Cost

- UB: Undistributed Budget (activities not yet distributed to control account)

- WP: Work Package (near-term, detail-planned activities within a control account)

At start of Construction Stage

During Construction Stage

Notes

1 If authorized as part of TPC.

2 During execution, contingency moves into the PMB per change control process.

3 Favorable > 0, Unfavorable < 0.

_______________________

cum=cumulative